Exits, risk & schedule

How the exploration tests stops and take-profits, risk rules and trading time windows.

Finding a good entry signal is only half the work. How and when you exit a trade defines most of the final result: a good setup with a poor exit loses money, and a mediocre setup with well-calibrated exits can be profitable. In this section you configure the three pillars that the exploration tests alongside the signals: exit modes (TP/SL), risk management rules and trading time windows. Like indicators, most of these parameters are swept by range (From / Steps / To), so the exploration tests different values and keeps the ones that work best.

TP/SL Management (exit modes)

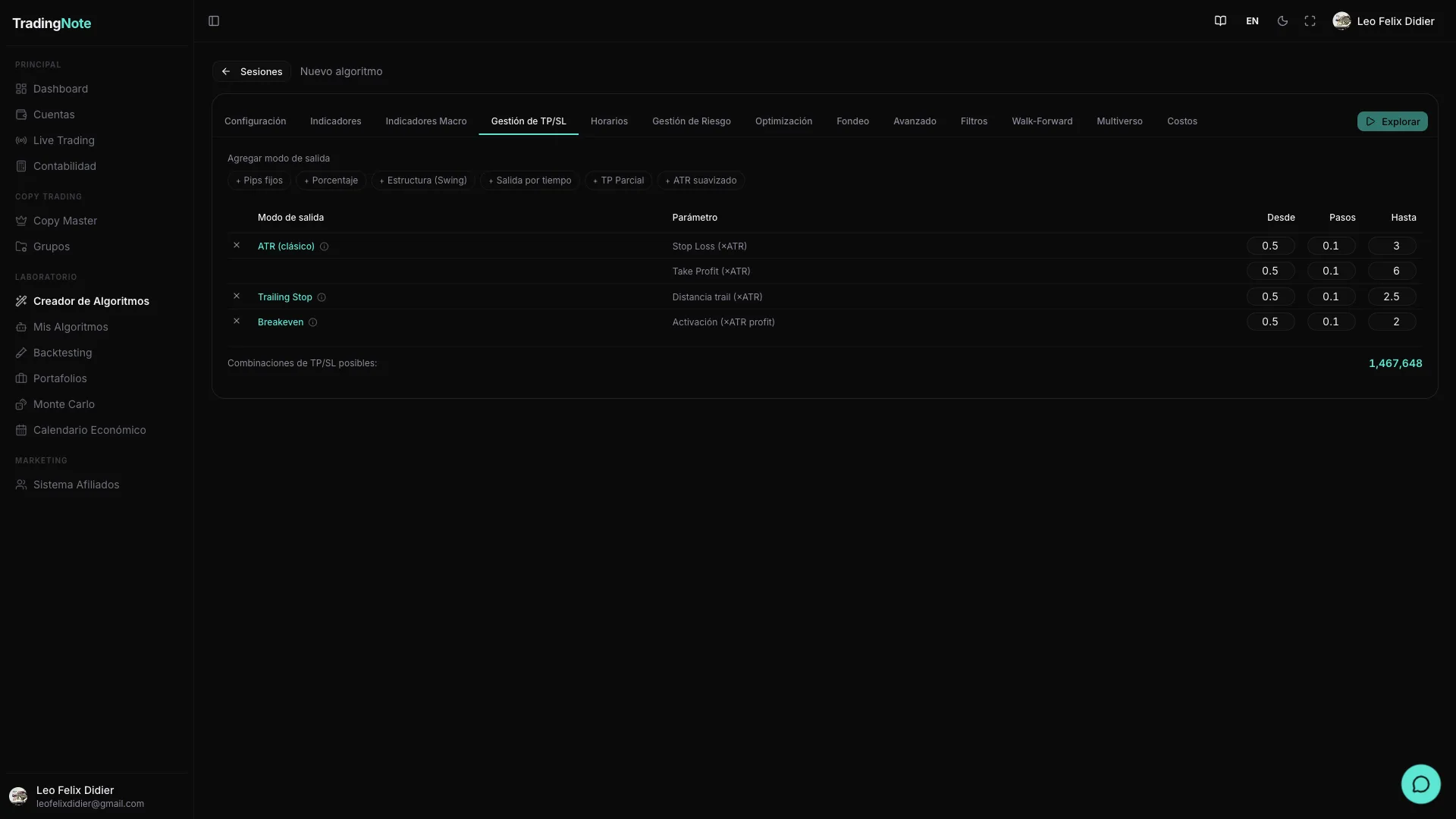

The exploration supports nine exit modes. You can enable several at once and the exploration tests which one performs best for each indicator combination. All numeric parameters (multipliers, distances, lookbacks) are swept over the range you configure: the platform automatically picks the optimal value within that range.

| Mode | What it does | Parameters & typical range |

|---|---|---|

| Classic ATR | Places the SL and TP as multiples of ATR(14). It is the most widely used mode: it adapts the exit distance to the recent volatility of the asset. | slAtr: 0.5–3.0 · tpAtr: 0.5–6.0 |

| Fixed pips | SL and TP at a fixed number of pips, regardless of volatility. Useful for assets with stable spreads and predictable volatility. | slPips: 10–50 · tpPips: 20–100 |

| Percentage | SL and TP as a percentage of the entry price. Scales automatically with the asset price. | slPct: 0.2–2 % · tpPct: 0.5–4 % |

| Trailing Stop (ATR) | The SL follows the price towards profit keeping a fixed ATR distance. Lets profits run while still protecting open trades. | trailAtr: 0.5–2.5 |

| Breakeven | When the trade has X·ATR of profit, moves the SL to the entry price. Turns a winning trade risk-free. | beActivationAtr: 0.5–2.0 |

| Structure (swing) | Places the SL at the low (long) or high (short) of the last N candles. Respects price structure instead of an arbitrary distance. | lookback: 10–50 candles |

| Time exit | Closes the trade after N candles regardless of the result. Prevents a trade from staying open indefinitely. | maxBars: 5–50 |

| Partial TP | Closes a fraction of the position at TP1 (closer) and the rest continues to TP2 (further). Locks in partial profit and lets the remainder run. | tp1Atr: 0.5–2 · tp2Atr: 2–6 · partialPct: 30–70 % |

| Smoothed ATR | Same as classic ATR but uses the average of ATR(14) over the last 50 candles. Reduces the impact of one-off volatility spikes. | slMult: 0.5–3 · tpMult: 1–6 |

You can enable multiple modes at once: the exploration tests each one independently and shows you which mode performed best for each algorithm. Start with classic ATR plus Trailing Stop for a solid baseline.

Risk management

Risk rules determine when the algorithm stops trading: maximum daily, weekly or total losses, profit limits and per-trade operational controls. Configuring them correctly is critical if you plan to trade a real or funded account: the exploration applies them during the backtest, so the results you see already respect those limits.

| Rule | Category | What it limits | Typical range |

|---|---|---|---|

| maxDailyGainPct | Gains | Maximum profit in a single day. When reached, the algo stops opening new trades that day. | 1–5 % |

| maxWeeklyGainPct | Gains | Maximum profit in a week. Stops trading for the rest of the week when reached. | 2–10 % |

| maxMonthlyGainPct | Gains | Maximum profit in a month. When reached, the algo does not open new trades until next month. | 5–20 % |

| maxAccountGainPct | Gains | Total account profit target. When equity exceeds this percentage above the initial balance, the algo stops. | 10–50 % |

| maxConsecutiveWins | Gains | Stops the algo after N consecutive wins. Prevents trading in overconfidence mode. | 3–10 |

| maxDailyLossPct | Losses | Maximum loss in a single day. When reached, the algo opens no new trades that day. It is the most important limit for funded accounts. | 1–5 % (prop firms: 2–5 %) |

| maxWeeklyLossPct | Losses | Maximum loss in a week. When reached, the algo stops for the rest of the week. | 2–10 % |

| maxMonthlyLossPct | Losses | Maximum loss in a month. If reached, the algo opens no more trades until next month. | 5–20 % |

| maxAccountLossPct | Losses | Maximum total allowed account drawdown. If equity falls more than this percentage from the initial balance, the algo stops permanently. | 5–20 % (prop firms: 6–12 %) |

| maxConsecutiveLosses | Losses | Stops the algo after N consecutive losses. Protects against loss streaks in adverse market conditions. | 3–10 |

| riskPerTrade | Operational | Percentage of capital risked on each trade. Controls lot size together with the SL distance. | 0.5–3 % |

| rewardRiskRatio | Operational | Minimum accepted TP/SL ratio. The exploration discards trades whose risk-reward ratio falls below this value. | 1–5 |

| maxOpenTrades | Operational | Maximum number of simultaneously open trades. Prevents the algo from accumulating unlimited exposure in fast market conditions. | 1–5 |

| maxDailyTrades | Operational | Maximum number of trades the algo can open in a single day. Controls overtrading on high-signal-activity days. | 1–20 |

If you plan to trade a funded account (prop firm), set maxDailyLossPct and maxAccountLossPct to your challenge limits from the start. This way the backtest results already reflect what the algorithm can earn while respecting those rules, not in an infinite-risk vacuum.

Schedule (trading sessions)

Financial markets do not have the same liquidity or volatility at all hours. Restricting trading to the asset's natural session typically improves signal quality and reduces false trades. The exploration tests your algorithm only within the time window you configure.

| Session | Time (UTC) | Notes |

|---|---|---|

| 24 hours | 00:00–24:00 (no restriction) | The algo trades at any hour. Recommended only if the asset has continuous liquidity (crypto) or you already filter by other rules. |

| Sydney | 21:00–06:00 UTC | Low liquidity on most assets. AUD and NZD see slightly more activity. High spreads on pairs unrelated to the Pacific. |

| Tokyo | 00:00–09:00 UTC | JPY, AUD and NZD are active. JPY cross pairs have their best movement here. Moderate volume on Asian indices. |

| London | 07:00–16:00 UTC | Highest volume in forex. EUR, GBP and CHF see peak activity. Includes the first 4 hours of NY, with a high-liquidity overlap. |

| New York | 12:00–21:00 UTC | Dominant session for USD, US indices (USTEC, US30, SPX) and commodities like gold. High activity around US macro data. |

| Tokyo-London overlap | 07:00–09:00 UTC | Short window but with elevated volatility. Good for breakout strategies on JPY and European pairs. |

| London-NY overlap | 12:00–16:00 UTC | Maximum liquidity of the day. The 4 hours with the highest volume across all markets. Ideal for strategies that need clean movement and tight spreads. |

Additional schedule rules

In addition to the time window, you can enable specific rules that the exploration applies as additional conditions on when the algorithm may trade:

- closeBeforeNyClose: closes all open positions before 21:00 UTC (NY close). Useful for not holding positions overnight during low-liquidity sessions.

- closeBeforeWeekend: closes all open positions on Friday at 20:00 UTC. Avoids Sunday gap risk when markets reopen.

- noNewTradesFriday: opens no new trades on Friday. Already open positions continue their normal management; no new entries are generated.

- noMondayOpen: does not trade until 01:00 UTC on Monday. Gives the market time to absorb the Sunday gap before entering.

- avoidRollover: avoids the 20:55–21:10 UTC window where brokers apply swaps and the order book may have abnormal price jumps.

Restricting the trading hours usually improves trade quality: many strategies only work well in their natural session. An algorithm designed around the US dollar makes sense in the London-NY overlap, not at 03:00 UTC with triple spreads. If your exploration generates few trades, widen the time range; if it generates many of low quality, restrict to the highest-liquidity session for that asset.

Closing positions before the weekend avoids Sunday gap risk but cuts the number of trades and can penalize strategies with longer holds. It is a deliberate trade-off, not an absolute truth: evaluate with and without the rule and compare results before deciding.

Next step

Once you have configured exits, risk and schedule, the exploration is ready to run. When it finishes, candidate algorithms will go through robustness filters (DSR, Walk-Forward and Multiverse) and you will be able to adjust real commission costs. Continue in «Optimization, funding & costs» to understand that phase.